Use the Standard Formula to Calculate Debt Payments

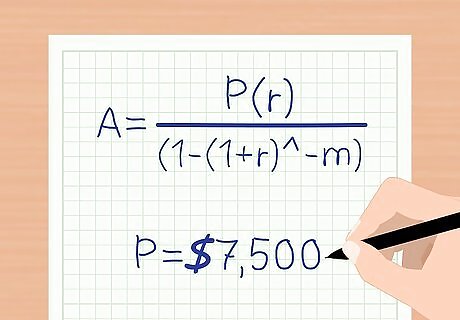

Understand the standard formula used to determine the monthly payments on a loan. Payments can be calculated using the following equation: A = P ( r ) ( 1 − ( 1 + r ) − m ) {\displaystyle A={\frac {P(r)}{(1-(1+r)^{-m})}}} A={\frac {P(r)}{(1-(1+r)^{{-m}})}}. In the equation, the variables stand for the following: A is the monthly payment amount. P is the principal. r is the monthly interest rate. m is the number of months on the loan.

Get the principal of the loan. The principal of the loan is the amount that you're borrowing. For example, if you're borrowing $7,500, then the principal is $7,500. This value will be P in the equation you use to calculate the monthly payment.

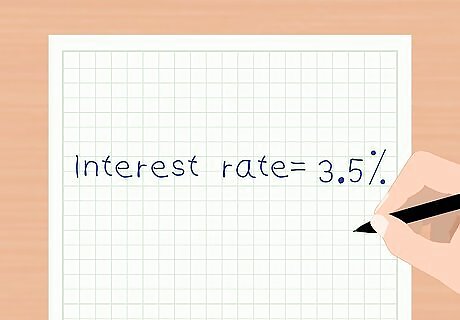

Determine the interest rate. The interest rate is basically the expense you'll pay the lender in exchange for borrowing the money. You'll be given the interest rate when you take out the loan. It's usually expressed in terms of an Annual Percentage Rate (APR), such as 3.5 percent. This number represents the percent interest charged on the principal over the course of a year.

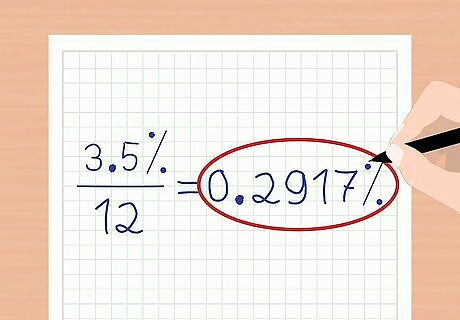

Calculate the monthly interest rate. You need the monthly interest rate because your payments are on a monthly basis but the interest rate is on an annual basis. The interest rate is calculated by simply dividing the annual interest rate divided by 12. For example, if the annual interest rate is 3.5 percent, then the monthly interest rate is .2917 percent (3.5/12). This value will be r in the equation you use to calculate the monthly payment. The monthly interest rate must be entered as a decimal, so first we must divide by 100 to get the decimal form of .2917%, which is 0.002917. This will be the r variable in the equation.

Get the length of the loan, in years. Most loans are over a period of years. That's the amount of time that you have to pay back the loan.

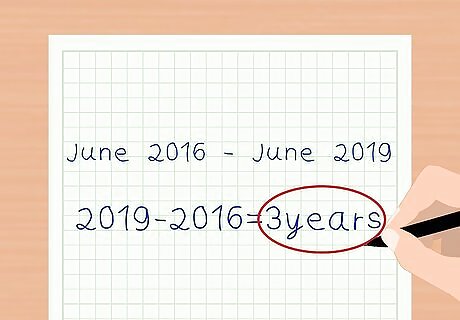

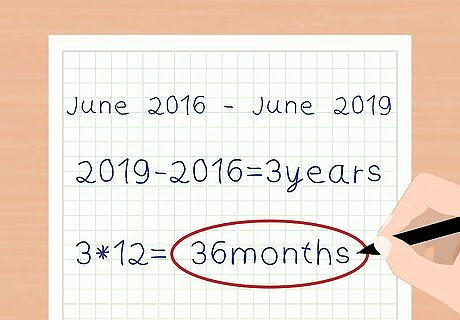

Calculate the number of months in the loan. The number of months in the loan is easy to calculate because it's the number of years in the loan times 12. For example, if the loan is 3 years long, then the number of months in the loan is 36 or 3 x 12. This value will be m in the equation you use to calculate the loan.

Calculate monthly payments. Input your variables into the equation and solve. Suppose, using the numbers from above, that the principal is $7,500, the interest rate is 3.5 percent per year (or .2917 percent per month), and the number of months given to repay the loan is 36 (3 years). The complete equation using these numbers is as follows: A = $ 7 , 500 ( 0.002917 ) ( 1 − ( 1 + 0.002917 ) − 36 ) {\displaystyle A={\frac {\$7,500(0.002917)}{(1-(1+0.002917)^{-36})}}} A={\frac {\$7,500(0.002917)}{(1-(1+0.002917)^{{-36}})}} The first step would be to add the number in parentheses (1+0.002917) to get: A = $ 7 , 500 ( 0.002917 ) ( 1 − ( 1.002917 ) − 36 ) {\displaystyle A={\frac {\$7,500(0.002917)}{(1-(1.002917)^{-36})}}} A={\frac {\$7,500(0.002917)}{(1-(1.002917)^{{-36}})}} Then, solve the exponent (^-36) to get: A = $ 7 , 500 ( 0.002917 ) 1 − 0.9005 {\displaystyle A={\frac {\$7,500(0.002917)}{1-0.9005}}} A={\frac {\$7,500(0.002917)}{1-0.9005}} Note that this result (0.9005) is rounded. You can keep more decimals place to keep your final answer more accurate. Continue by multiplying the principal by the rate to get: A = $ 21.88 1 − 0.9005 {\displaystyle A={\frac {\$21.88}{1-0.9005}}} A={\frac {\$21.88}{1-0.9005}} Then solve the subtraction. This gives: A = $ 21.88 0.0995 {\displaystyle A={\frac {\$21.88}{0.0995}}} A={\frac {\$21.88}{0.0995}} Divide the final two numbers to get your answer: A = $ 21.88 0.0995 = $ 219.90 {\displaystyle A={\frac {\$21.88}{0.0995}}=\$219.90} A={\frac {\$21.88}{0.0995}}=\$219.90 Your answer, $219.90, is your monthly payment on your 3-year, $7,500 loan at 3.5 percent.

Use a Spreadsheet to Calculate Debt Payments

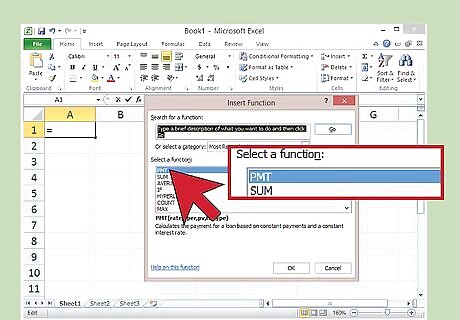

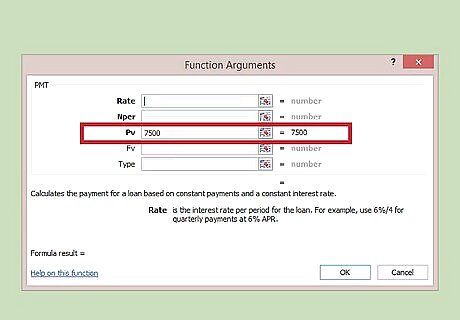

Locate the "Payment" function on your favorite spreadsheet software. Your spreadsheet software will almost certainly have a "Payment" function. You'll use that function to calculate the loan payments based on the particulars about the loan.

Get the principal of the loan. The principal of the loan is the amount that you're borrowing. For example, if you're borrowing $7,500, then the principal is $7,500.

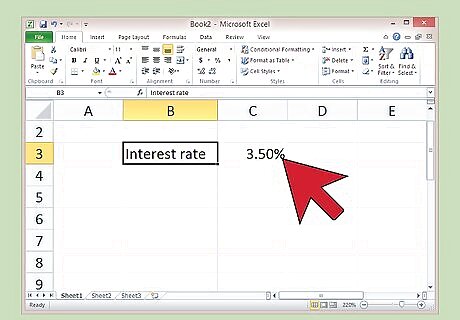

Determine the interest rate. The interest rate is basically the expense you'll pay the lender in exchange for borrowing the money. You'll be given the interest rate when you take out the loan. It's usually expressed in terms of a percentage, such as 3.5%.

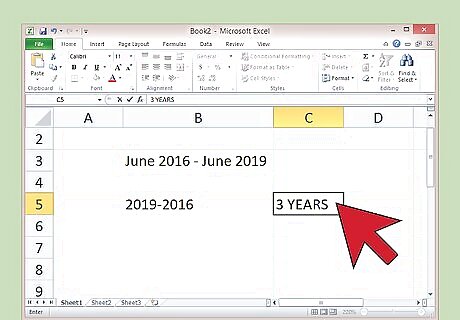

Get the length of the loan, in years. Most loans are over a period of years. That's the amount of time that you have to pay back the loan.

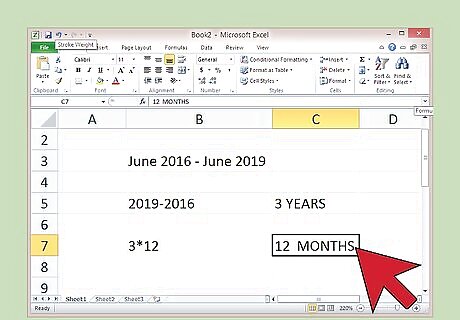

Calculate the number of months in the loan. The number of months in the loan is easy to calculate because it's the number of years in the loan times 12. For example, if the loan is 3 years long, then the number of months in the loan is 36 or 3 x 12.

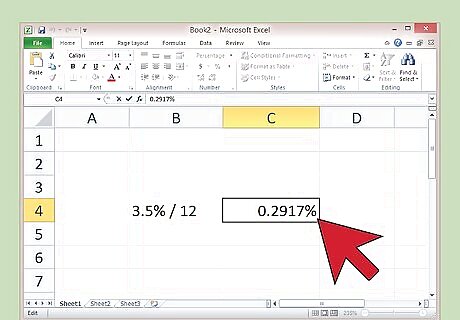

Calculate the monthly interest rate. You need the monthly interest rate because your payments are on a monthly basis but the interest rate is on an annual basis. The monthly interest rate is calculated by simply dividing the annual interest rate divided by 12. For example, if the annual interest rate is 3.5 percent, then the monthly interest rate is .2917 percent. Your interest rate will have to be entered in decimal form. To get this, divide the percent form (0.2917) by 100. This gives 0.002917.

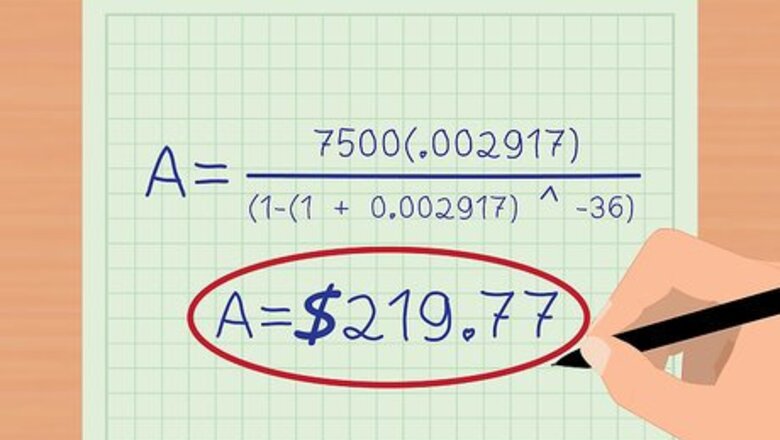

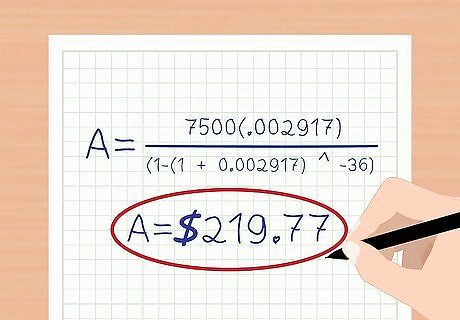

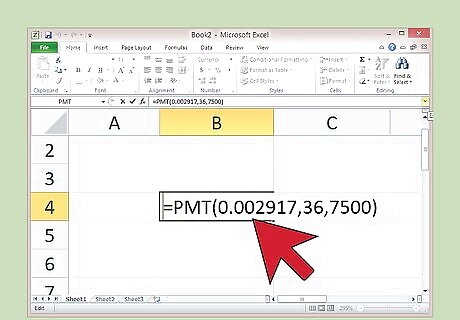

Use the payment function to calculate the payment. You'll plug in the principal, rate, and number of months into the payment function. Consult the documentation for your spreadsheet software to determine exactly how to plug in those numbers. Once you've plugged in the numbers, the resulting value will be the payment. If you use the numbers mentioned above, the payment value should be $219.77. Using Microsoft Excel, you'll use the PMT function. The first value in the function is the rate, the second value is the number of months, and the third value is the principal of the loan. For this example, the PMT function in this case looks like this: =PMT(0.002917,36,7500).

Comments

0 comment