Beginning the Payment Agreement

Find a sample on the Internet and use it as a guide. You should search the Internet for a sample payment agreement that you could use as a guide as you draft your own. Each industry has its own standard payment agreements which might differ from the information in this article. For example, if you are drafting a student loan repayment agreement, then its contents would differ substantially from the information provided here.

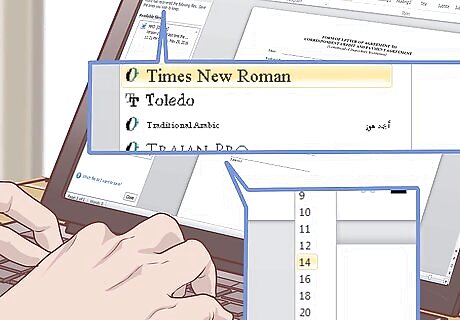

Format your document. You can begin drafting your payment agreement by opening a blank word processing document and setting the font to a readable size and style. The exact font and size does not really matter, as long as it is readable and looks professional. Times New Roman 12 or 14 point works for most people. Avoid fonts that are smaller than 10 point, as they may be too hard to read. Avoid fonts that are larger than 14 point; it is unnecessary and will waste paper. Choose a professional-looking font face, such as Times New Roman or Arial. Skip the handwritten fonts, such as Comic Sans. Although legible, they look unprofessional.

Add a title. Put the title in bold and in all caps, so that it stands out, but use the same font face. Center the title between the left- and right-hand margins. You can do this by highlighting the title, then choosing the center-alignment option in your program. Consider making the title slightly bigger than the rest of your font. For example, if you used 12 point font throughout your document, try 14 point for the title. Keep the title simple. You can title the note “Payment Agreement” or “Loan Agreement.”

Identify the parties. You need to identify the person making the loan, who is the “lender,” and the person borrowing the loan, who is the “borrower.” You should also include information about the date of the loan here. For example, you could write: “This loan agreement (‘Agreement’) dated this 12th day of August, 2015, made between Michael Smith, of Chicago, IL (‘Lender’) and Amy Jones of Detroit, MI (‘Borrower’).”

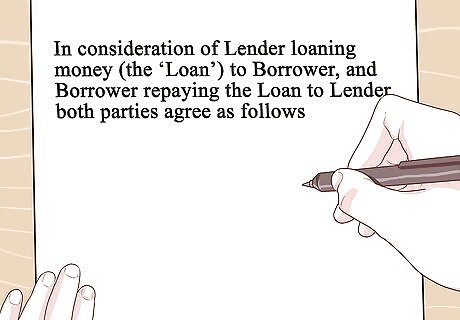

Include your consideration. You don’t have a valid loan until both the borrower and the lender agree to do something in exchange for the other person doing something in return. You should state what each side agrees to do. For example, you can write: “In consideration of Lender loaning money (the ‘Loan’) to Borrower, and Borrower repaying the Loan to Lender, both parties agree as follows.”

Explaining the Terms of the Loan

Identify the loan amount and interest. The first thing you should include is the amount of the loan and the interest rate. Your state has probably set a maximum interest rate you can charge as well, which you can find online. If you want to charge interest, research your state and federal laws. For example, the IRS requires that you charge a minimum interest rate, otherwise, they may interpret the loan as a “gift” for tax purposes. Sample language could read: “Lender promises to loan $5,000 USD to Borrower. Borrower promises to pay back this amount to Lender, with interest payable on the unpaid principal at a rate of 4% per annum, calculated yearly not in advance.”

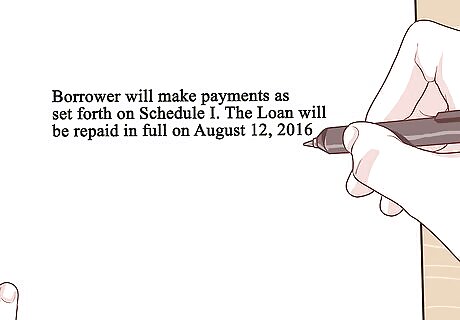

Explain the schedule of payments. You should include the date the loan will be paid in full. You also might want to attach to your payment agreement a schedule listing when monthly payments are due. On your schedule, list the day of each payment and the amount that the borrower should pay. If you aren’t charging interest, then divide the amount by the number of monthly payments. Sample language could read: “Borrower will make payments as set forth on Schedule I. The Loan will be repaid in full on August 12, 2016.”

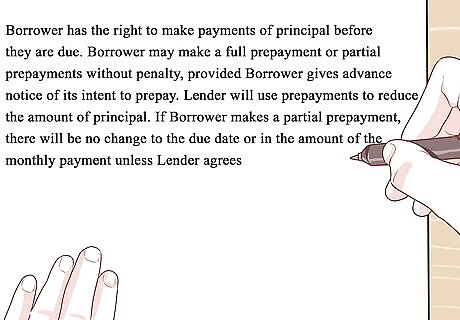

Grant a right to prepayment. The borrower might find that he or she can pay off the loan early. You should explain in the payment agreement whether this is allowed. Generally, prepayment is a good deal for the lender because he or she will get the money paid back early; however, the lender would lose out on some interest. A sample prepayment provision could read: “Borrower has the right to make payments of principal before they are due. Borrower may make a full prepayment or partial prepayments without penalty, provided Borrower gives advance notice of its intent to prepay. Lender will use prepayments to reduce the amount of principal. If Borrower makes a partial prepayment, there will be no change to the due date or in the amount of the monthly payment unless Lender agrees.”

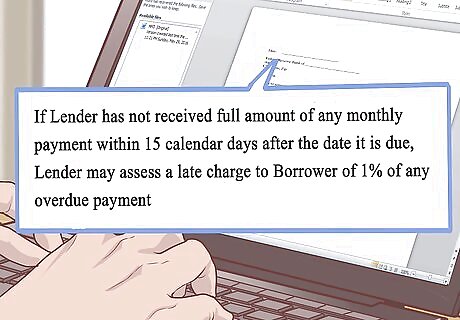

Explain any late charges. The seller might want to charge a penalty or additional interest if the borrower is late with payment. You should explain what the late charge will be and how you will calculate it. For example, if you want to charge a percentage penalty, you could write: “If Lender has not received full amount of any monthly payment within 15 calendar days after the date it is due, Lender may assess a late charge to Borrower of 1% of any overdue payment.”

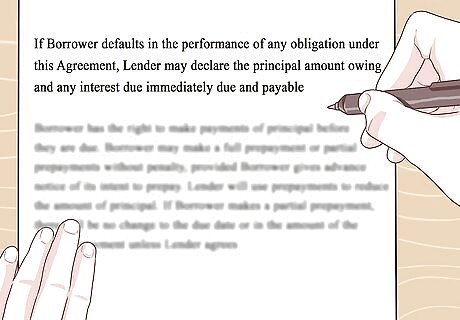

Identify default. “Default” occurs when the borrower does not follow the terms of the payment agreement. Typically, the borrower will default when he or she misses a payment. However, the lender usually reserves the right to declare a default. The lender usually reserves the right to immediately demand payment of all outstanding principal and interest. Sample language: “If Borrower defaults in the performance of any obligation under this Agreement, Lender may declare the principal amount owing and any interest due immediately due and payable.” With this provision, the lender doesn’t have to declare a default, but he or she has the option if payment is missed.

Finalizing the Payment Agreement

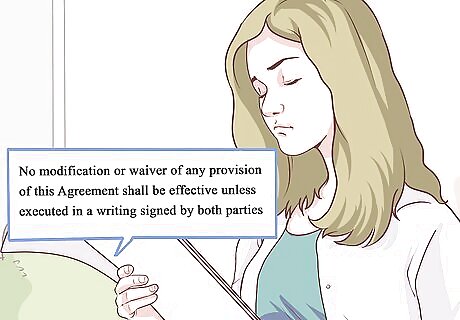

Identify how to modify the agreement. You might decide to change the terms of the loan after signing. In this situation, you will need to modify the payment agreement. You should include a provision that explains how you can modify the agreement. Sample language could read: “No modification or waiver of any provision of this Agreement shall be effective unless executed in a writing signed by both parties.”

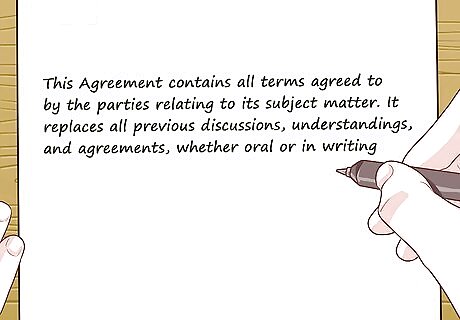

Explain that this represents the entire agreement. You don’t want one party claiming at a later date that there were oral side agreements. For this reason, include a provision stating that the written payment agreement represents the entire agreement. For example, you could write: “This Agreement contains all terms agreed to by the parties relating to its subject matter. It replaces all previous discussions, understandings, and agreements, whether oral or in writing.”

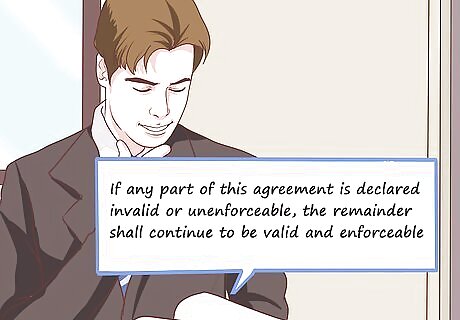

Add a severability clause. If there is a lawsuit, then the judge might find that one provision of your payment agreement is illegal. The judge could potentially then strike down the entire payment agreement. To prevent this from happening, you should include a “severability provision.” A sample severability provision could read: “If any part of this agreement is declared invalid or unenforceable, the remainder shall continue to be valid and enforceable.”

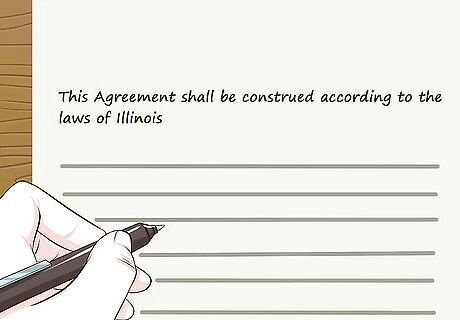

State the governing law. If a lawsuit breaks out, then the judge will need to interpret the contract according to some state’s law. You can decide which state’s law to apply. Generally, the lender decides to use the law of the state where they are located. You could write: “This Agreement shall be construed according to the laws of Illinois.”

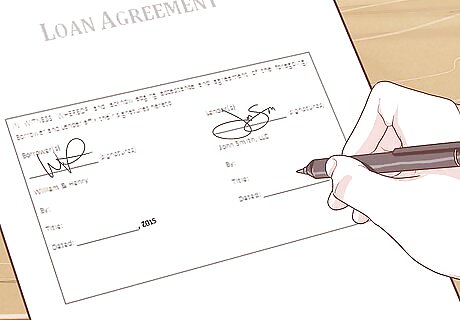

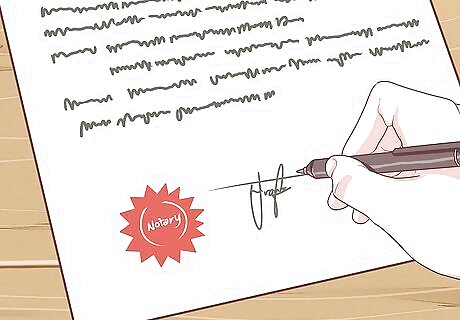

Insert signature blocks. Both the borrower and the lender should sign the agreement. Include signature lines for both. Under each line, include the following: Name Title Date

Include a notary block, if necessary. Your state might require that payment agreements be signed in front of a notary public. If so, you should search the Internet and find an acceptable notary block to insert beneath the signature lines. You can find notaries at most large banks, court houses, and city manager’s offices. As an alternative, you can also use the Locator feature at the website for the American Association of Notaries. You should take sufficient personal identification to show the notary. Generally, a valid driver’s license or passport should be sufficient.

Deciding Whether to Make a Loan

Analyze whether you can afford to lend. Many people decide to lend to family or friends in times of need. However, before you agree to lend money, you should check whether you can afford to. Ask yourself the following: Do you need to save additional money for retirement? If so, then lending might not be the best idea. Do you have debts yourself that you need to pay off? You could pay off your loans earlier if you don’t loan to friends or family. How important is it for you to be repaid and can you afford to make the loan? Loaning money to someone you know can put a serious strain on your relationship. If they are unable or refuse to repay the loan, you will have to weigh the importance of the relationship against your need or desire for repayment.

Ask why the borrower needs the money. Some loans never get repaid, and one important piece of information you should find out is why the borrower needs the loan. For example, the borrower might have unforeseen medical expenses or be struggling to pay off student loan debt. Even people who are careful with their money can rack up these debts. However, other people might be taking a loan to cover other loans. This is a sign that the person is in financial distress. Instead of making a loan, you should recommend that they see a credit counselor.

Consider non-loan alternatives. There might be ways you could help family and friends without giving them a loan. For example, you could let them borrow your car, if they have unmet transportation needs. You could also suggest that someone move in with you for a period of time. These might not sound like ideal situations, but they are less risky than giving a monetary loan, which might not be repaid.

Discuss the parameters of the loan. Once you have decided to loan or borrow money, you need to sit down with the other party to the agreement and discuss the terms of the loan. If you are borrowing money, be honest about your financial situation and when you can reasonably expect to begin repaying the loan. If you are lending money, set a hard limit on the amount that you are willing to lend and decide when you need the money repaid. If both parties state their needs and concerns, it is less likely that either party will resent the other party to the agreement.

Establish a repayment schedule. It is very important to agree to a repayment schedule that works for both parties. This will minimize resentment and tension regarding the borrowed money. By coming to an agreement on repayment, both the lender and the borrower should feel comfortable that the loan will be repaid. If you are borrowing money, do not overestimate how quickly you can repay the loan. Create a budget and plan how and when you can reasonably make the loan repayments. If you are lending money, determine how quickly you need the money back and whether you can make an extended loan so that the borrower has an easier time repaying you. You can calculate repayment schedules and interest using loan calculators online.

Comments

0 comment