Ensuring Corporate Responsibility

Establish an independent audit committee to oversee audits. SOX requires the boards of publicly traded companies (i.e., those listed on U.S. stock exchanges) to establish an independent committee that will be responsible for overseeing the external auditors tasked with making sure your company's finances are in order. This group of individuals will be in charge of hiring the company’s auditor, establishing the procedures that the auditor will abide by, determining compensation for the auditor, and ensuring that the auditor they hire will perform his or her job effectively. The audit committee members by law may not have any other relationship with the company and may not receive compensation for any other services performed for the company. It will be helpful if at least one of these members has experience or education relating to general accounting procedures, financial reporting, and the auditing process as a whole who can serve as a resource to the committee while it carries out its duties. Regardless, you must disclose whether or not your committee includes such an expert.

Change the lead and reviewing audit partners every five years. SOX requires that the individuals with the most influence over the auditing process be regularly cycled out for fresh individuals. This reduces the likelihood that any improper relationships develop that would compromise the integrity of the auditing process.

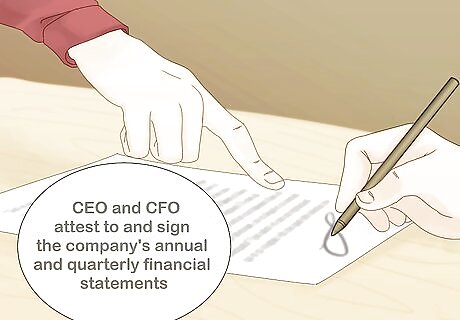

Get CEO and CFO signatures on annual and quarterly financial statements. It is important to have both your company's chief executive officer ("CEO") and chief financial officer ("CFO") attest to and sign your company's annual and quarterly financial statements. SOX requires these individuals to be ultimately responsible for these reports, and you must therefore ensure that these individuals are provided with the necessary information regarding your company's financials so that they can fulfill this requirement adequately. They will have to certify that: They have reviewed the financial report. The information contained therein is accurate and fairly presented. Such information is free from mistakes, misleading statements, and omissions of relevant facts.

Establish internal procedures and controls to ensure SOX-related compliance. Your CEO and CFO are responsible for the internal accounting controls. They are required to report any deficiencies in internal accounting controls or any fraud involving the management of the audit committee. Any material changes to internal accounting controls must be reported by the CEO and CFO. Of course, this step is vital to running any successful business, but it is even more important when those executives may be personally subject to consequences for failing to understand and sign off on these issues.

Have all members of your company adhere to blackout periods for stock trading. Employees cannot sell their stock purchased through the company’s 401K program during the blackout period.Such a blackout period usually occurs during administrative changes in the plan and lasts for several business days.

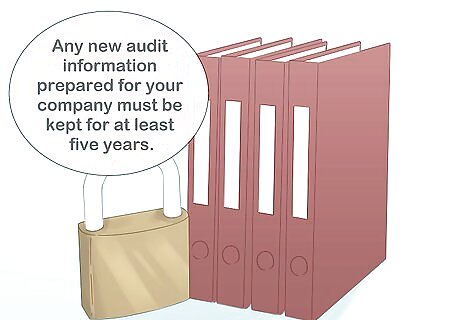

Treat your financial records with care. Any attempt to destroy, alter, omit, or falsify relevant financial information or records that would thwart a federal investigation or other relevant government proceeding is prohibited under SOX. Any new audit information prepared for your company must be kept for at least five years. You may be imprisoned for up to 20 years and have to pay fines for altering, destroying, concealing or falsifying records or documents with the intent to influence a federal investigation or bankruptcy case.

Hire a consultant or designate an internal employee to stay up to date on SOX-related rules and standards. These are issued by the Public Company Accounting Oversight Board ("PCAOB"). The PCAOB—a private-sector, nonprofit corporation created by SOX to oversee audits of publicly traded companies—sets forth requirements with which companies must comply. This employee should also monitor regulations issued by the Securities and Exchange Commission, which oversees the PCAOB and sometimes promulgates its interpretations of PCAOB rules.

Promoting Investor Confidence

Disclose all financial transactions and relationships. In addition to the financial dealings included in your company's balance sheet, any financial information that is off your company's balance sheet that could potentially affect your company's finances must be disclosed under SOX. As one of SOX's primary goals is to increase investor confidence and prevent corporate fraud, any information that affects your company's financial situation in a meaningful way should be disclosed. If you are in doubt, it is always best to disclose so that your compliance with SOX or motives are not called into question. SOX prohibits a company from providing personal loans to its directors or executive officers.This rule also extends to subsidiary companies.

Develop a code of ethics for your company's senior financial officers. While SOX does not explicitly require you to create such standards for your high-level executives, it does require you to disclose whether or not your company has this type of code in place.Having a robust system in place to govern the actions of the senior members of your company is a great way to promote transparency and demonstrate the your company is doing its best to comply with SOX's objectives. Any changes or waivers of the code must also be disclosed as they arise.

Develop a system by which employees can submit any information pertaining to internal fraud. This should be done by your independent auditing committee to preserve the integrity of this important process, and should be completely confidential. While you obviously will be doing your best to comply with the provisions of SOX, many companies are large in size and scope, and things can happen without management's knowledge. Having such a system in place will help your company remain on the level by allowing a certain degree of self-policing, as employees will feel they can do the right thing anonymously without fear of reprisal. Make sure this system is truly confidential, as any adverse action taken against an employee for this type of whistleblowing activity, or for aiding in a federal investigation, is strictly prohibited under SOX.

Inform your employees they will be protected if they engage in whistleblowing. Whistleblowers are people who alert the company when there has been a breach of internal policy and/or government regulations. A whistleblower cannot be fired as a result of whistleblowing. Demoting, denying overtime, benefits, or promotion to, disciplining, failing to hire or rehire, intimidating, unfavorably reassigning, or reducing pay or hours for such an employee is also prohibited under SOX. If your employees are assured they do not have to fear reprisal for reporting instances of fraud, they will be more likely to do so. This will help your company deal with problems quickly and privately, preserving your company's reputation and compliance with SOX. Make sure that your company has a reporting and investigation process in place for instances of whistleblowing.

Disclose any significant changes to your company's finances or operations. These changes must be disclosed rapidly after they arise in a manner a layperson could understand. As SOX concerns itself with investor confidence, this helps your investors keep abreast of changes to your company's financial status in more-or-less real time. Legal insider trading involving the company's directors or officers must be reported within two business days.

Comments

0 comment