X

Trustworthy Source

Internal Revenue Service

U.S. government agency in charge of managing the Federal Tax Code

Go to source

Withholding and Paying FICA Taxes

Total your employee's annual income. You are required to withhold and pay FICA taxes for your household employee if you pay them more than $2,100 in cash wages over the course of the year. Cash wages include money paid directly to the employee, but don't include in-kind compensation such as meals or lodging. For example, if you have a live-in nanny and pay him $200 a week, only the $200 weekly compensation is considered cash wages – not the value of the lodging or any food he may consume while in your home. In most cases, people who work in your household will be considered employees and subject to FICA withholding. However, if you have any doubts, you can file Form SS-8 and ask the IRS to make a determination. Download the form at https://www.irs.gov/pub/irs-pdf/fss8.pdf.

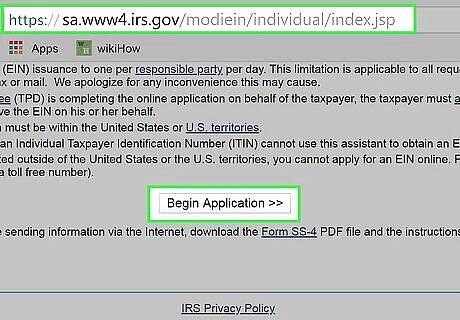

Request an employer identification number (EIN). You may already pay individual taxes under your Social Security number. However, if you're going to withhold and pay taxes for an employee, you need a separate EIN. The easiest way to get an EIN is online. Provide some basic information and your EIN will be issued immediately. Visit the IRS website at https://sa.www4.irs.gov/modiein/individual/index.jsp to get started.

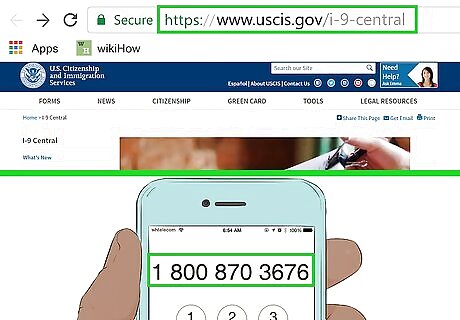

Complete and file Form I-9. Form I-9 is a U.S. Citizenship and Immigration Services (USCIS) form that proves your household employee can legally work in the United States. You will have to verify identification from your employee. Go to https://www.uscis.gov/i-9-central to download the form and instructions, or call 1-800-870-3676 and have one sent to you. You must keep a copy of Form I-9 in your records as long as the employee works for you.

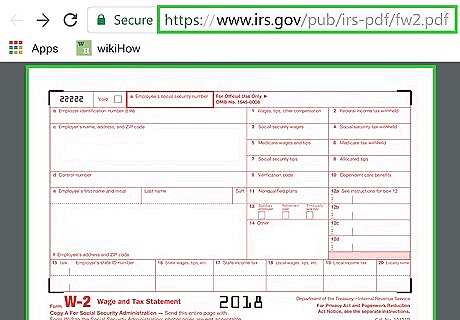

Complete Form W-2 each year. Use this form to report employee wages and taxes withheld for the year. Give your employee copies B, C, and 2 by January 31 of the following year. You can download a copy of Form W-2 at https://www.irs.gov/pub/irs-pdf/fw2.pdf. Make sure the form you download is dated for the year you want to report.

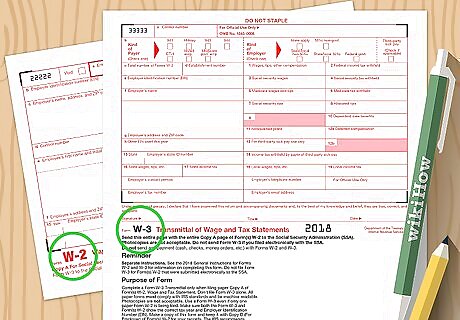

File Form W-2 with Form W-3. Form W-2, along with a completed transmittal form, must be submitted to the Social Security Administration (SSA) by January 31 of the next year. The easiest way to file is online. If you file online, you don't have to complete a separate Form W-3. The SSA will generate this form when you file your W-2. You also must use the scannable file available directly from SSA to file a W-2 with the SSA. You cannot use the copy available for download from the IRS. Visit https://www.ssa.gov/employer/ to register for the SSA's online business services. There is no charge for using any of these services.

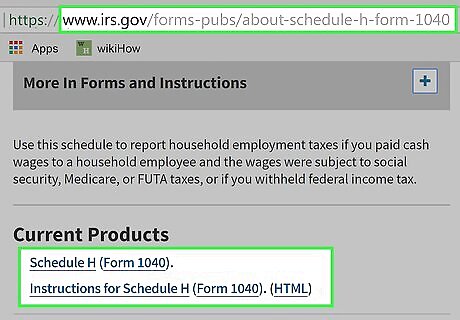

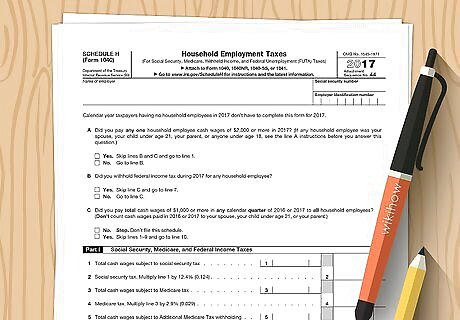

Complete Schedule H with your annual tax return. When you file your taxes each year, fill out and attach Schedule H to calculate your tax liabilities for your household employees. If you use tax preparation software, the schedule will be completed based on your answers to simple questions. You can download the Schedule H form and instructions at https://www.irs.gov/forms-pubs/about-schedule-h-form-1040. If you're not required to file Form 1040, but you still owe taxes for a household employee, you can sign and file Schedule H separately.

Make estimated tax payments if necessary. If you anticipate you will owe more than $1,000 in taxes at the end of the year, you are required to make quarterly estimated tax payments. If you end up owing $1,000 or more come tax time, you may also be hit with an estimated tax underpayment penalty. If you're not sure how much you'll potentially owe in taxes, you can use the worksheet that accompanies Form 1040-ES to estimate your tax liability. Download the form and instructions at https://www.irs.gov/pub/irs-pdf/f1040es.pdf. If you have a full-time job, you also may instruct your employer to withhold additional money for your taxes, rather than paying separate estimated taxes each quarter. If you're not withholding federal or state income taxes for your household employee, advise them that they also may have to make quarterly estimated tax payments on their income.

File your annual tax return as usual. Having household employees doesn't change the way you normally pay taxes. When you file your 1040, you'll also file Schedule H that details what you paid your household employees. If you've been paying quarterly estimated taxes, you shouldn't owe any additional money come tax time. If you do owe taxes as a result of household employee taxes not covered by any quarterly estimated tax payments you made, you can pay these taxes online or through your tax preparation software, just as you normally would.

Paying FUTA Taxes

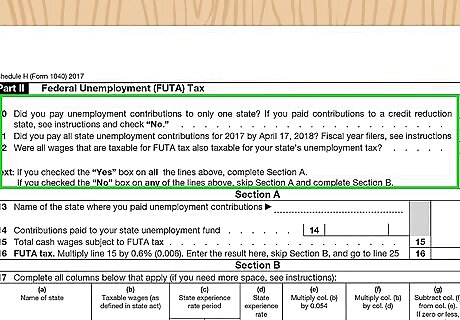

Total your payments to all household employees on Schedule H. Generally, you are required to pay Federal Unemployment (FUTA) taxes at the rate of 6 percent on the first $7,000 of wages paid to household employees. If you only have one household employee and pay them less than $1,000 in any quarter, you aren't required to pay FUTA taxes. However, if you have more than one household employee, you pay FUTA taxes based on the total amount you paid to all of them, even if you paid one employee less than $1,000 a quarter. When you total payments made to household employees, you should also include payments to any employees that don't meet the threshold ($1,000 or more in a quarter). However, you don't have to include payments made to people working in your household who are not considered employees, such as family members or full-time students under the age of 18.

Report your contributions to your state's unemployment fund. If you pay all required contributions to your state unemployment fund by the yearly tax deadline, you can use those payments as a credit against your FUTA taxes. Provided all your contributions were made by the deadline, you can take a credit of up to 5.4 percent against the FUTA tax. This gives you an effective rate of 0.6 percent for FUTA taxes to be paid with your annual return. Your credit amount may be reduced if you are in a credit reduction state. These are states identified by the U.S. Department of Labor that haven't repaid money borrowed from the federal government to pay unemployment benefits. These states change every year, and are listed in the instructions for Schedule H.

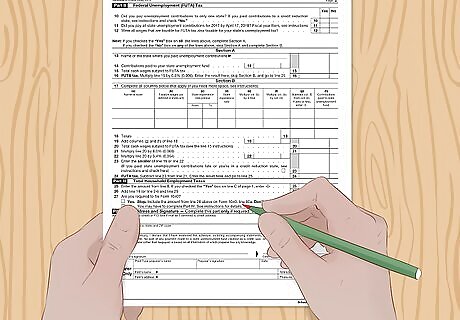

Pay FUTA taxes with your annual return. After completing Schedule H, you'll enter the amount of FUTA taxes you owe, if any, on line 60a of your 1040. This amount becomes part of your overall federal tax liability, and may be reduced by any deductions or credits you claim, as well as any estimated tax payments you made throughout the year. If you aren't required to file a Form 1040 tax return, but you still paid household employees, you can sign and file Schedule H separately and pay whatever amount is owed.

Assessing Your State Tax Liability

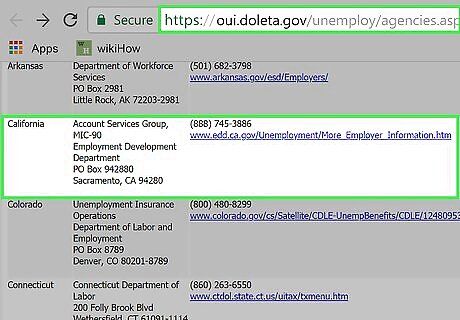

Contact your state's unemployment tax agency. If you have a household employee and are paying federal taxes on them, you are likely also responsible for making contributions to your state's unemployment fund. To determine your liability, contact your state's unemployment tax agency. The U.S. Department of Labor has a list of each state's unemployment tax agency with links to their websites at https://oui.doleta.gov/unemploy/agencies.asp.

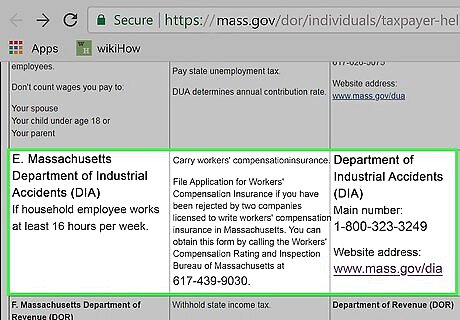

Obtain worker's compensation insurance if necessary. Many states require you to carry worker's compensation insurance for your household employees. This requirement typically kicks in if you pay them more than a threshold amount, or they work for a minimum number of hours. For example, you are required to carry worker's compensation insurance in Massachusetts if you have a household employee who works at least 16 hours a week. Contact your state's department of labor to find out if worker's compensation is required in your circumstances. Generally, you can get worker's compensation insurance from any insurance agency or broker that handles business insurance.

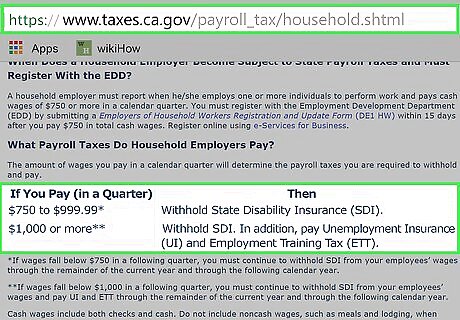

Withhold state taxes as necessary. Your state may have additional taxes, such as state disability taxes, that you are required to withhold from your household employee's wages. Your state tax agency will be able to provide more information. Most states don't require you to withhold state income taxes for your household employees, but you can if you and your employee agree to do so. Otherwise, your employee will likely be on the hook for quarterly estimated taxes.

File quarterly reports. Most states require you to file quarterly reports with the state's unemployment tax agency that identify your employees and the amount of money they earned during that quarter. You may also be required to file similar reports with your state's department of revenue, even if you're not withholding income taxes from your household employee's paychecks. The business center of your state's department of revenue will be able to give you more information about what reports you need to file.

Comments

0 comment