Calculating Personal Net Income

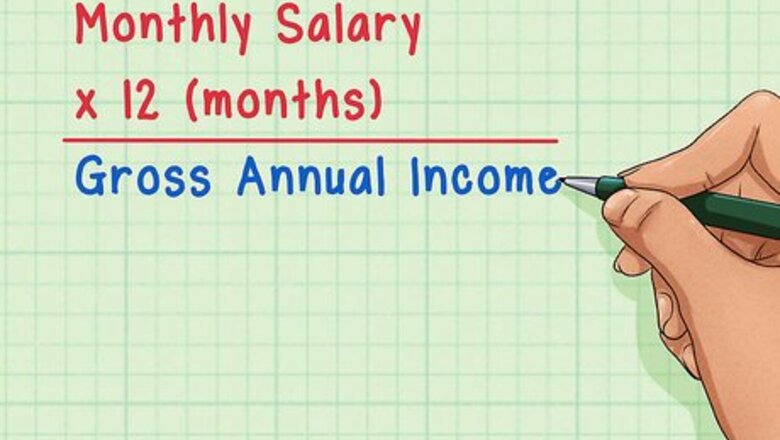

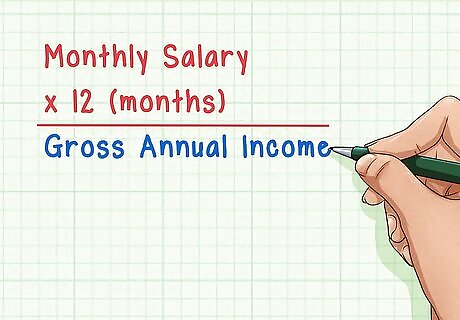

Calculate your gross annual income. Your first step to calculating your net income is finding out your gross income. Gross income is the total amount of money you make in a year before taking taxes or deductions into account. It serves as your starting point for calculating net income. If you are on a salary or work stable hours, this should be fairly easy to calculate. Take a pay stub from one of your pay periods. If your employer takes out taxes, look at the total amount before the deductions. This is your gross pay for the period. Figure out how often you are paid, and multiply the gross pay accordingly. If you're paid monthly, multiply the number from your pay stub by 12 to get your gross annual income. If you're paid weekly, multiply it by 52. If bi-weekly, multiply by 26. If you work irregular hours, you'll have to add up all your pay stubs for the year to get an accurate measure of your annual income. If you work multiple jobs, take all of them into account in this calculation. In most cases, gifts and inheritance do not factor into gross income. These are still taxable, however, so remember to account for them when filing your taxes.

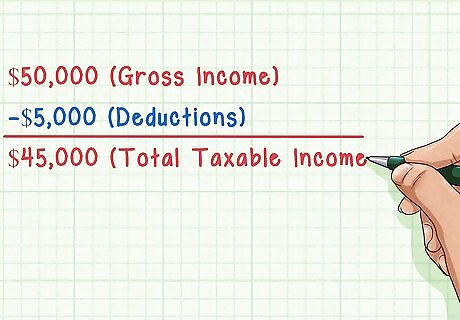

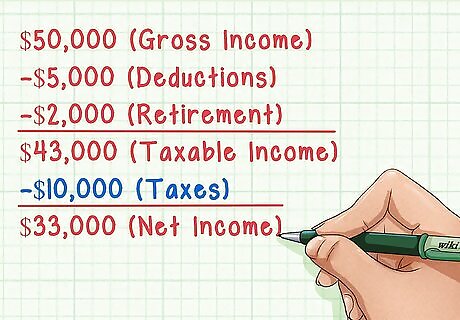

Subtract any deductions you have. Since net income refers only to your income after taxes, you have to subtract any deductions you have from your gross annual income. After you subtract any deductions from your gross income, then you'll end up with your total taxable income. For example, if you had a gross income of $50,000 and $5,000 in deductions, then your taxable income is $45,000.

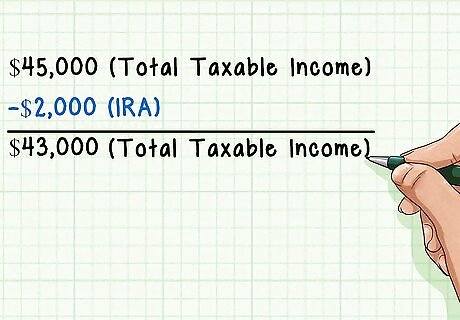

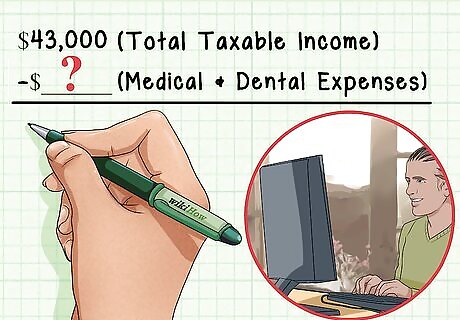

Deduct your retirement contributions if applicable. Under certain circumstances, your individual retirement arrangement (IRA) can be deducted from your taxable income. This will vary depending on your particular arrangement, so consulting the IRS webpage will help you discern if you can make any deductions based on your retirement savings. Let's say, for example, that you're allowed to deduct $2,000 from your taxable income. That means that your taxable income falls from $45,000 to $43,000.

Deduct your medical and dental expenses if applicable. As with retirement savings, you can sometimes deduct medical and dental expenses from your taxable income. This varies depending on your particular situation, so consult the IRS webpage for information on whether or not you can deduct your medical expenses.

Subtract what you owe in taxes from your annual pay. After you've found out what your total taxable income is, then you have to subtract the amount you owe in taxes. Add up all taxes you owe, including federal, state, local, Medicare and social security. If your employer takes out taxes, then the total deductions should be on your pay stubs. Subtract the total taxes from your income to get your net annual income. Sticking with the previous example: if your gross income was $50,000, you had $5,000 in deductions, and you deducted another $2,000 for retirement, your taxable income is $43,000. Then if you owe $10,000 in taxes, that makes your net income $33,000. If at any point you're confused about your taxes, consulting an accountant will help clear things up.

Calculating Business Net Income

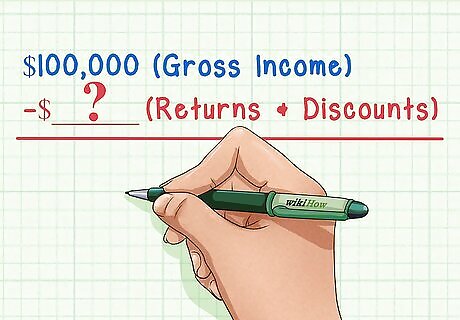

Add up your gross income for the last year. For businesses, net income refers to profit after expenses and taxes. To start, gather your records and add up your total income for the past year, before taxes or expenses. Subtract returns and discounts from your gross income. Self-employed people should follow this method because they have to deduct their own taxes from payments. Let's say that your net gross income, before expenses, was $100,000. That will serve as your gross income for this part.

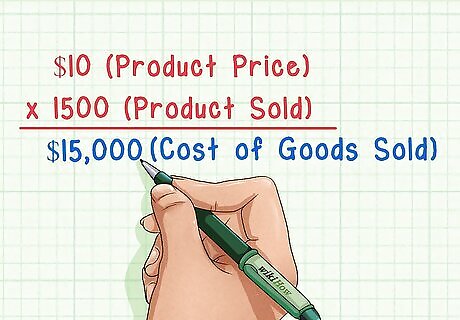

Add up the cost of goods sold. If your business involves selling products, then you have to account for what those products originally cost. Multiply the price of each unit by the number of units sold. Then subtract this total from the total income. The result is your "Operating Income." If you sold 1,500 products and each cost you $10, then your cost of goods sold is $15,000. Remember this total for the example below. If your business provides a service, you can skip this step. Any materials you use to provide the service falls under operating costs.

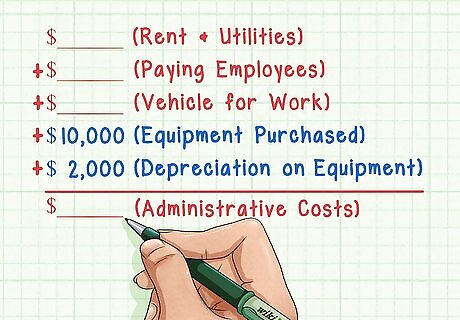

Add up your administrative costs. In this step, you will add up all of your expenses in operating your business. They may vary from business to business, but there are a few costs that are common and must be accounted for. Rent and utilities. If your business has a storefront, then you probably pay rent and utilities. Paying employees. If you use a vehicle for work, the cost, gas, taxes, insurance, and maintenance on it goes into your operating costs. Purchase of any equipment you used. Depreciation on equipment. Depreciation refers to an asset that loses value over time. For example, if you buy a piece of equipment for $10,000 and expect it to last five years, then it depreciates by $2,000 a year. Factor this into your calculations for gross income. For more information on calculating depreciation, read Account For Accumulated Depreciation.

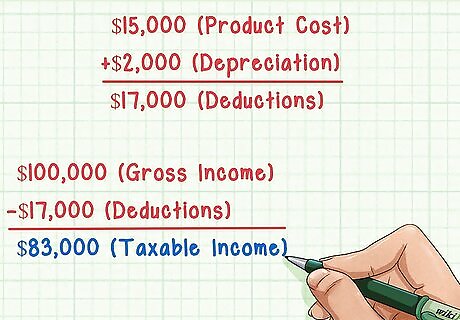

Compute your taxable income. After you add up your product cost and administrative expenses, you can come to your taxable income. Add up your cost of goods, administrative expenses, and other deductions. Then subtract that number from your net gross income. That should leave you with your taxable income. The numbers given in this part were $15,000 for your product cost and $2,000 in depreciation. This is a total of $17,000 in deductions. Since your original net gross income was $100,000, an $17,000 deduction would give you a taxable income of $83,000.

Calculate what you owe in taxes. Based on your taxable income, you can figure out what you owe in taxes. This number will vary widely depending on your income, the size of your business, the amount of equipment you have, and so on. For help, it is best to refer to guidelines from the US Small Business Administration.

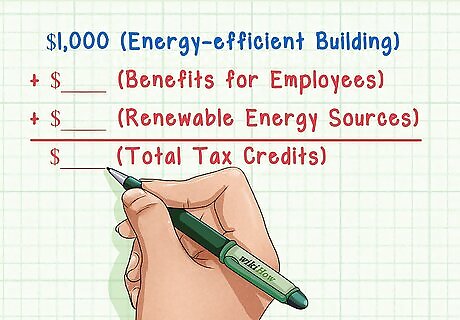

Add up any tax credits you have. Federal and local governments grant numerous tax breaks for businesses. Things like having an energy-efficient building, providing benefits for employees, and using renewable energy sources may qualify you for a tax break. Visit the IRS site for a complete list of tax breaks from the federal government. Let's say the federal government gives you a $1,000 tax credit for having an energy-efficient building. You can subtract this amount from the total of taxes owed. It will make this step much easier if you have an accountant. She will be well-versed in tax law and know how best to calculate your taxes. For more tips, read Prepare for Small Business Tax.

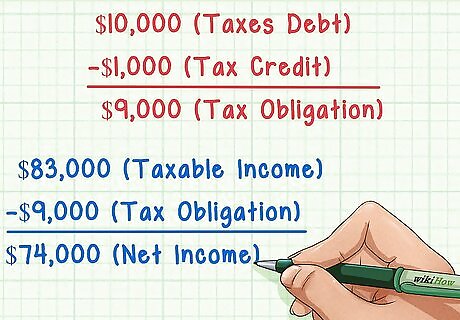

Subtract your tax obligations from your taxable income. After you figure out what you owe in taxes, subtract that number from your taxable income. Once you do this, then you've arrived at your business net income. Let's say that you figure out you owe $10,000 in taxes, but you have that $1,000 tax credit, so you owe $9,000. Subtract that from your taxable income of $83,000 and you get a final net income of $74,000.

Comments

0 comment