Understanding Investing Basics

Look at your investment choices. Intrinsic value is used to measure the true value of an investment, so it’s important to understand the basics of investing. A company has two ways to raise money to run the business. They can issue stock or bonds. Companies issue common stock by selling ownership in the business. When you buy stock, you are an owner (investor) in the business. Your shares of stock represent a small percentage of ownership in the company. A bond represents a company debt. Investors who buy bonds are considered business creditors. The bond owner receives interest income on the bond investment, usually twice a year. The original amount invested is returned to the bond investor on the maturity date.

Consider how a business becomes profitable. Intrinsic value is based on the ability of a business to generate cash flow into the company and earn a profit. When a company’s revenue (or sales) are higher than their expenses, the firm generates earnings. For this discussion, you can think of earnings and profit as the same thing. Companies must use cash to buy inventory, make payroll and advertise. That type of spending is considered a cash outflow. When customers pay for a product or service, the business has a cash inflow. The ability to generate more cash inflows than outflows over time indicates a valuable company.

Choose an investment option. Investors have hundreds of investment choices. A bond investor, for example, expects a certain amount of interest income. A stock investor is interested in seeing the value of stock increase over time or in receiving a share of the earnings in the form of dividends. The intrinsic value formulas make assumptions about an investor’s required rate of return You can think of this return as the investor’s minimum expectation. If the investment cannot meet the expectation, it’s assumed that an investor would not invest.

Using the Dividend Discount Model

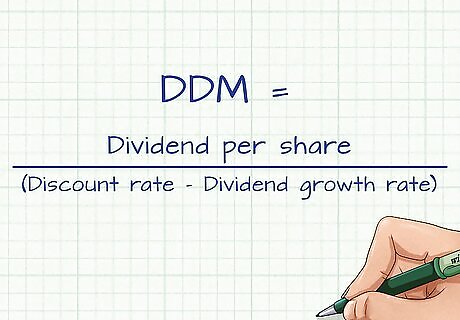

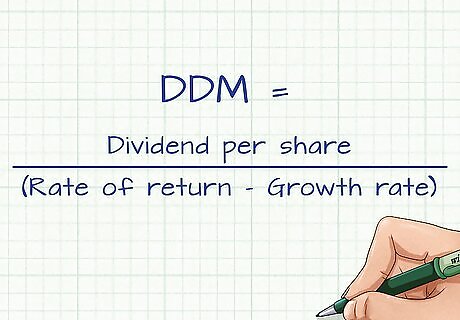

Understand the definition. The dividend discount model (DDM) considers the dollar value of dividends paid to shareholders. This model also factors in a projected growth rate of the dividend. Dividends are discounted to their present value using a discount rate. If the dividend discount model values the stock at a higher price than the current market value, the stock’s price is considered to be undervalued. The DDM formula is (Dividend per share)/ (Discount rate – Dividend growth rate).

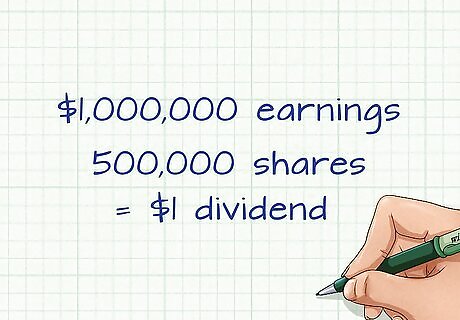

Consider the growth rate for dividends. A dividend is a payment of a company’s earnings to shareholders. If a company’s earnings are expected to grow, an analyst may also assume that the dividends paid to shareholders may grow. You should assume a growth rate for the DDM formula. Say, for example, that your company has earnings for the year of $1,000,000. You decide to pay $500,000 to shareholders in the form of a dividend. If your firm had 500,000 shares of common stock outstanding, you would pay a $1 dividend on each share of stock. Assume that the company earns $2,000,000 in the following year. The firm may decide to pay a larger dollar amount as a dividend- say $1,000,000. If the number of common stock shares is still 500,000, each share of stock would receive a $2 dividend.

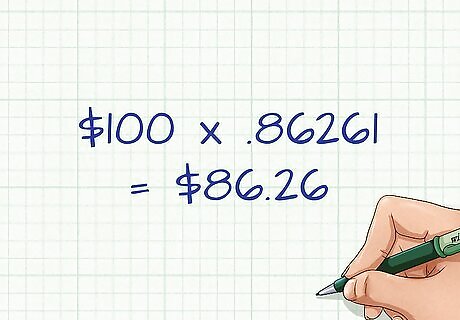

Apply a discount rate. The discount rate is the percentage rate used to discount future payments into today’s dollars. Discounting payments to the current day allows the analyst to make a “apples to apples” comparison of cash flows from different periods of time. Remember that, for this formula, the discount rate is the rate of return required by the investor. It should take into account the stability of the dividend payment. For example, if the dividend payment is erratic, the discount rate should be higher. Assume that you expect to receive a $100 payment in five years. Assume also that the discount rate each year will be 3%. You can use a present value table to determine the present value factor for $100 received in 5 years, at a discount rate of 3%. The factor is .86261 (Other tables or calculators may be slightly different, due to rounding). The present value of the payment is ($100 multiplied by .86261 = $86.26).

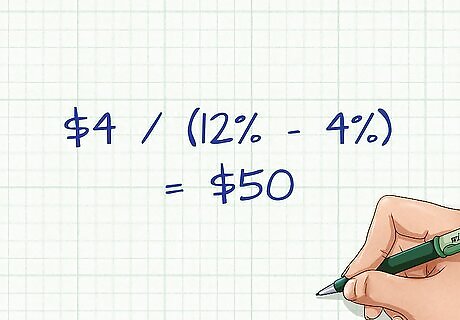

Input your assumptions into the DDM formula. The DDM formula is (Dividend per share)/ (Discount rate – Dividend growth rate). Dividend per share is the dollar amount of dividend paid for each share of common stock. Assume the dividend is $4 per share. The discount rate is the investor’s required rate of return. Assume a 12% discount rate. Assume a 4% percentage rate of dividend growth each year. The DDM formula is ($4 / (12% - 4%) = $50). If the current market price of the stock is less than $50 per share, the formula indicates that the stock price is undervalued. In other words, the intrinsic value of the stock is higher than the stock’s current price.

Considering the Gordon Growth Model

Analyze the concept of dividend growth in perpetuity. Many companies grow their sales and earnings over time. If earnings grow, the firm has the option of paying more earnings to shareholders as a dividend. The Gordon Growth Model makes an assumption that dividends will grow at a specific rate forever. The formula is (Expected dividend per share, one year from today)/ (Investor required rate of return - Growth rate in dividend in perpetuity).

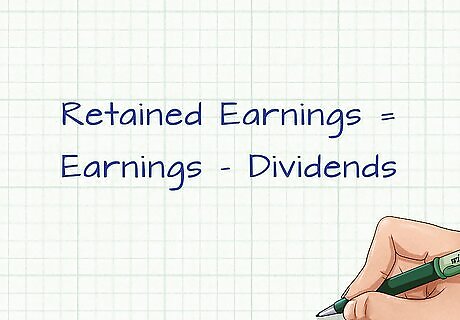

Understand that a business can pay earnings as a dividend to shareholders, or can keep the earnings for future business use. Earnings kept by the company are referred to as retained earnings. A company's balance in retained earnings is the sum of all earnings less all dividends paid since the business started.

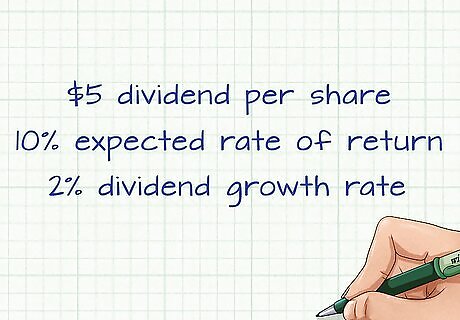

Make some assumptions for the variables in the formula. Assume the company’s expected dividend per share one year from now is $5. Decide on an expected rate of return required for an equity (stock) investor of 10%. Make an assumption that the annual dividend growth rate in perpetuity is 2%.

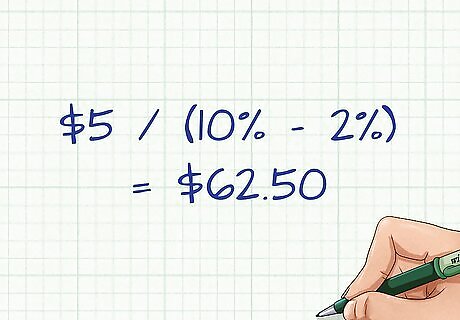

Use the formula to calculate intrinsic value. The Gordon Growth Model would be ($5 / (10% - 2%) = $62.50). $62.50 is the intrinsic value of the stock, using this model. If the current market price of the stock is less than $62.50, the model indicates that the stock is undervalued.

Applying the Residual Income Formula

Look at book value per common share. Book value is defined as a company’s assets – liabilities. It can also be defined as a firm’s equity. If a company sold all of the assets and used the available cash to pay off all remaining liabilities, any cash left over would be considered equity (book value).

Understand the concept of residual value. A company has book value as a starting point. The formula then adds new (expected) earnings that the company generates over and above a required rate of return. You’re adding “extra value” to the existing book value of the stock. If the company can grow earnings at a faster rate than required, the firm will be more valuable. If the calculation’s intrinsic value is more than the current market value, the stock is undervalued.

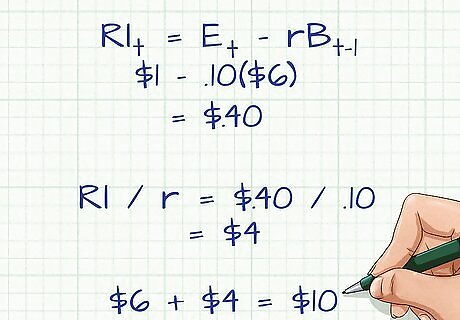

Add in residual value. The formula for residual value has two components. It is the current book value of the equity plus the present value of future residual income. For example, suppose a company will earn $1.00 per share forever, and the company also pays out all of this as dividends, $1.00 per share. The equity capital invested (book value) is $6.00 per share. Because the earnings and dividends will offset each other, the future book value of the stock will always stay at $6.00. The required rate of return on equity (or the percent cost of equity) is 10 percent. Calculate the annual residual income with the formula R I t = E t − r B t − 1 {\displaystyle RI_{t}=E_{t}-rB_{t-1}} RI_{t}=E_{t}-rB_{{t-1}}, where R I t {\displaystyle RI_{t}} RI_{t} = residual income in future periods; r {\displaystyle r} r = required rate of return on equity, E t {\displaystyle E_{t}} E_{t} = net income during period t {\displaystyle t} t. If the net income is $1.00 per year, the book value is always $6.00 and the required return is 10 percent, the the annual residual income is $ 1.00 − .10 ( $ 6.00 ) = $ 1.00 − $ .60 = $ .40 {\displaystyle \$1.00-.10(\$6.00)=\$1.00-\$.60=\$.40} \$1.00-.10(\$6.00)=\$1.00-\$.60=\$.40 The present value of future residual income is R I t / r = $ .40 / .10 = $ 4.00 {\displaystyle RI_{t}/r=\$.40/.10=\$4.00} RI_{t}/r=\$.40/.10=\$4.00 The intrinsic value is the current book value plus the present value of future residual income. The equation is $ 6.00 + $ 4.00 = $ 10.00 {\displaystyle \$6.00+\$4.00=\$10.00} \$6.00+\$4.00=\$10.00. The intrinsic value is $10.00

Implementing the Discounted Cash Flow Method

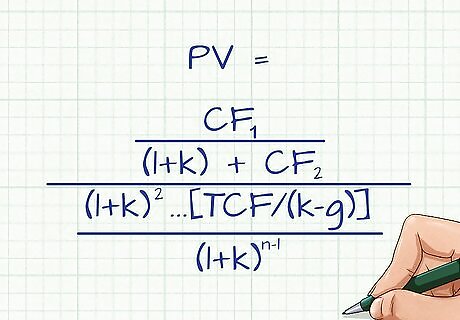

Learn the formula. The formula for the discounted cash flow method is: P V = C F 1 / ( 1 + k ) + C F 2 / ( 1 + k ) 2 {\displaystyle PV=CF_{1}/(1+k)+CF_{2}/(1+k)^{2}} PV=CF_{1}/(1+k)+CF_{2}/(1+k)^{2}… [ T C F / ( k − g ) ] / ( 1 + k ) n − 1 {\displaystyle [TCF/(k-g)]/(1+k)^{n-1}} [TCF/(k-g)]/(1+k)^{{n-1}}. P V {\displaystyle PV} PV = present value C F i {\displaystyle CF_{i}} CF_{i} = cash flow in year i k {\displaystyle k} k = discount rate T C F {\displaystyle TCF} TCF = terminal year cash flow g {\displaystyle g} g = growth rate assumption in perpetuity beyond terminal year n {\displaystyle n} n = the number of years in the period including the terminal year. To understand the formula, you need to understand free cash flow, capital expenditures and weighted average cost of capital.

Consider free cash flow. Free cash flow is defined as operating cash flow less capital expenditures. Operating cash flow is the cash inflows and outflows from your day-to-day business. That includes buying inventory, making payroll and collecting cash from customers. A capital expenditure represents your spending on fixed assets, such as machinery and equipment. Think about the assets you will use in your business over a period of years. Successful companies are able to generate most of their cash from operations. If you manufacture and sell denim jeans, for example, selling jeans should be your primary sources of cash. If you have free cash flow, you have the flexibility to spend cash on areas that can grow your sales and earnings. If a competitor’s business was up for sale, for example, a firm could use their free cash flow to buy the operation and expand the company.

Go over weighted average cost of capital (WACC). Capital represents money you raise to run your business. If you issue stock to investors, they will expect some rate of return on their equity investment. Bond investors want an interest rate paid on their bond investment. Issuing bonds (debt) and stock (equity) comes with a cost. We refer to that cost as the cost of capital. If the profit you expect to generate on a project is more than the cost of capital, it makes financial sense to raise capital for a project. The discounted cash flow method uses WACC in the formula.

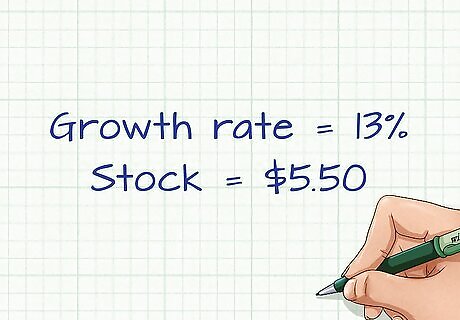

Plug in assumptions to the discounted cash flow (DCF) formula. Consider the valuation of Sun Microsystems in 2012. It was traded at $3.25. But the long-term growth rate was estimated to be 13 percent. This means the stock was valued at $5.50, making the $3.25 price a very good deal. Changes in the growth rate and interest rates have a huge impact on valuation.

Comments

0 comment